May 15, 2026

Remortgage Advice in Edinburgh: When Should You Switch Deals?

Most Edinburgh homeowners who are paying more than they should on their mortgage are not doing so because they made a bad decision. They are doing so because they made a perfectly sensible decision a few years ago, that decision expired, and nobody reminded them to review it.

When a fixed-rate mortgage ends, lenders automatically move borrowers onto their Standard Variable Rate (SVR). As of March 2026, the average SVR across major UK lenders stands at 6.83%, according to Compare the Market. For an Edinburgh homeowner with a £250,000 outstanding balance, sitting on an SVR of 6.83% instead of a competitive two-year fix could mean paying several hundred pounds more per month than necessary.

Remortgage Edinburgh timing matters. This guide explains when to act, what the Edinburgh market means for your options, and what a switch actually involves in Scotland's legal system.

What Is a Remortgage and Why Does It Matter in Edinburgh?

A remortgage means switching your existing mortgage to a new deal, either with your current lender or with a different one. It is not the same as moving home. You stay in the same property. What changes is the interest rate, the lender, the term, or some combination of all three.

For Edinburgh homeowners, remortgaging carries particular relevance in 2025 for two reasons.

- Edinburgh property values have grown substantially. The ONS records the average Edinburgh house price at £295,000 in February 2026, up 3.1% in the year and representing growth of approximately 51% since 2015, according to Statista's analysis of ONS data. ESPC data for July to September 2025 shows the Edinburgh, Lothians, Fife and Borders average selling price at £298,933, up 4.3% year on year. Homeowners who bought five or more years ago have, in many cases, moved into a meaningfully lower LTV band as their property has appreciated. That improved LTV position unlocks better remortgage rates they may not know are available to them.

- Rates have moved significantly since 2021 and 2022 fixed deals were taken out. Many Scottish homeowners who fixed in 2021 or 2022 at historically low rates of 1% to 2% have already come off those deals, or will do so in 2025. Moving onto an SVR of 6.83% from a 1.5% fix represents a substantial monthly increase. Reviewing options early, ideally three to six months before a deal ends, gives borrowers time to secure a new rate without unnecessary cost.

When Should You Remortgage in Edinburgh?

The right time to consider a remortgage Edinburgh review is not a single moment. It is a set of circumstances, and several of them apply to a large portion of Edinburgh homeowners right now.

Your current fixed-rate deal is ending within six months

This is the most straightforward trigger. When a fixed-rate period ends, the lender moves you onto its SVR automatically. The SVR is almost always higher, sometimes significantly higher, than the rate you were on. You do not need to wait for the deal to end before acting. Most lenders allow you to secure a new rate up to six months in advance, so your new deal begins the moment the current one expires with no gap on the SVR.

Starting the remortgage process six months before expiry is not cautious overcalculation. It is the standard recommended window. Mortgage offers typically remain valid for three to six months, and applications take time to process, particularly if you are switching lenders.

You are already on your lender's SVR

If your fixed-rate period has already ended and you have not switched, you are likely paying more than you need to. The question is not whether to remortgage but how quickly. A remortgage broker Edinburgh can assess the current market and identify products that would reduce your monthly payments immediately.

Every month spent on an SVR at 6.83% rather than a competitive fixed rate is a month of overpaying. On a £220,000 outstanding balance, the difference between 6.83% and 4.5% over 20 years works out to over £280 per month. Over 12 months on the SVR, that is more than £3,360 in unnecessary cost.

Your Edinburgh property has increased significantly in value

Edinburgh's house price growth since 2015 has moved many homeowners into a better LTV position than they were in when they originally mortgaged. Mortgage rates are structured in LTV bands. A homeowner who originally borrowed at 85% LTV and whose property has risen in value may now sit at 70% or 65% LTV. Those lower LTV bands attract meaningfully lower rates.

A remortgage with a new valuation reflecting Edinburgh's current prices can unlock the rates available at a lower LTV, even if the outstanding balance has not changed much. The ESPC House Price Report for April to June 2025 recorded Edinburgh's average selling price at £307,412, with Edinburgh City Centre rising 8.8% to £336,840. Homeowners in Leith, Portobello, Morningside, and Marchmont who have owned for five or more years may be sitting on substantial equity gains they have not yet used to improve their mortgage terms.

You want to release equity for home improvements or other purposes

Equity release through remortgaging is one of the most cost-effective ways to fund significant expenditure. Borrowing against your property at a mortgage rate is considerably cheaper than a personal loan or credit card.

Edinburgh property's consistent value growth means many homeowners hold substantial equity. A homeowner who bought at £220,000 in 2018 and whose property is now worth £295,000 has seen their equity grow by £75,000, even before accounting for mortgage capital repayments. A remortgage can release a portion of that equity as cash for a loft conversion, kitchen extension, or other improvements that may add further value to the property.

The Jones Whyte legal guide to remortgaging in Scotland gives the example of an Edinburgh homeowner releasing £30,000 for a loft conversion through a remortgage. At mortgage rates, the cost of borrowing that £30,000 is a fraction of what a personal loan would cost over the same term.

You want to consolidate debts

Some Edinburgh homeowners use a remortgage to consolidate unsecured debts, such as credit cards, personal loans, or car finance, into their mortgage. Mortgage rates are lower than rates on unsecured credit, so the monthly payment on consolidated debt is often considerably lower.

Debt consolidation through remortgaging has important caveats. Unsecured debts converted to secured mortgage debt are backed by your property. Extending the repayment period for short-term debts over a longer mortgage term increases the total interest paid, even at a lower rate. A remortgage broker Edinburgh should model the full-term cost of consolidation before it is treated as a straightforward saving.

Your circumstances have changed

A change in income, employment structure, or family situation can affect the mortgage products available to you, and in some cases open better options than were available when you originally mortgaged.

If you were previously self-employed with limited trading history and are now able to show two or more years of accounts, your lender choice is wider. If your income has grown substantially, you may qualify for higher borrowing at a lower LTV that changes your rate tier. If you have paid down debts, your affordability assessment improves. All of these are reasons to review your mortgage position even if your current deal has not yet ended.

How Edinburgh's Property Market Affects Your Remortgage Options

The Edinburgh market creates specific remortgage opportunities that homeowners in other parts of the UK do not have to the same degree.

LTV improvement through price growth

Edinburgh's 51% price growth since 2015 means that homeowners who bought before 2020 have, in most cases, moved through one or more LTV bands without making any extra payments beyond their standard repayments. A homeowner who bought a £200,000 property in 2016 with a 10% deposit (90% LTV) and whose property is now worth £295,000, with an outstanding balance of perhaps £155,000, now sits at approximately 53% LTV. That is a fundamentally different position in the eyes of a lender, with access to much lower rates.

The ESPC July to September 2025 data shows Edinburgh properties achieving an average of 102.4% of Home Report valuation, confirming that the market is still active enough to support strong remortgage valuations.

Rate environment context

The Bank of England cut its base rate to 3.75% in December 2025, according to Investropa's Edinburgh property analysis. Mortgage rates have edged lower as lenders compete for business in an improving market, with analysts expecting further movement through 2026. Edinburgh homeowners remortgaging in 2025 are doing so at rates that are lower than the 2023 peaks while equity positions remain strong.

Green mortgages

Some lenders now offer preferential rates on remortgages for properties that meet certain energy efficiency standards, or for homeowners using part of the remortgage to fund energy improvements. Older Edinburgh tenements and Victorian properties commonly have lower EPC ratings, and some Scottish lenders are specifically targeting this with green mortgage products. A broker familiar with the Edinburgh market can identify whether a green mortgage product applies to your property.

How Remortgaging Works in Scotland

The Scottish legal system introduces specific steps to remortgaging that differ from the process in England. Understanding these differences prevents unnecessary surprises.

You need a Scottish solicitor

Unlike in England, where remortgaging can sometimes be handled entirely by the lender's legal team, Scottish remortgages require a solicitor to handle the title registration and security transfer. Your solicitor updates the standard security (the legal document securing the mortgage against your property) and registers the new arrangement with the Registers of Scotland.

Solicitor fees for a Scottish remortgage are typically lower than for a purchase, usually in the range of £300 to £600, since no property conveyancing is required. Your remortgage broker Edinburgh can recommend solicitors experienced in Scottish remortgage transactions.

The standard security process

In Scotland, your mortgage lender holds a standard security over your property. When you remortgage to a new lender, the old standard security must be discharged and a new one registered in favour of the incoming lender. Your solicitor handles both steps. This process typically takes two to four weeks once the new mortgage offer is in place.

Product transfers with existing lenders

If you stay with your current lender and simply move to a new product (called a product transfer), the process is simpler. No new standard security is required and no solicitor is typically needed. Product transfers are faster and have lower associated costs, but they limit you to your current lender's product range. A whole-of-market comparison may identify better rates elsewhere.

A remortgage broker Edinburgh can compare your current lender's product transfer options against the full market, so you know whether staying or switching produces the better outcome for your specific balance, LTV, and income profile.

Early Repayment Charges

If you want to switch deals before your current fixed-rate period ends, your lender will almost certainly charge an Early Repayment Charge (ERC). ERCs are typically calculated as a percentage of the outstanding balance, often 1% to 5% depending on how far into the deal you are and which lender you are with.

In some circumstances, paying an ERC to exit a higher rate deal and move to a significantly lower one makes financial sense, particularly if the remaining ERC period is short. A broker can model whether the saving from switching early outweighs the cost of the charge.

What to Consider When Choosing a New Deal

When your Edinburgh remortgage review identifies that switching makes sense, the product decision involves several variables.

Fixed rate versus tracker

A fixed rate gives you certainty. Your monthly payment does not change regardless of what happens to the Bank of England base rate during the fixed period. In a period of rate uncertainty, that predictability has real value for household budgeting.

A tracker mortgage moves with the base rate. When the base rate falls, your payment falls. When it rises, your payment rises. Trackers typically have no ERCs, giving flexibility to exit if rates move against you. With the base rate currently at 3.75% following the December 2025 cut and analysts expecting further movement through 2026, trackers carry more appeal than in a rising rate environment, but they carry risk.

Two-year versus five-year fix

A two-year fix gives you a lower rate and flexibility to review again in 24 months. A five-year fix provides longer certainty but commits you to that rate for longer, which matters if you are planning to move, extend, or make major changes within five years.

The right choice depends on your plans for the property. Edinburgh homeowners who are planning to sell or upsize within two to three years are typically better served by a shorter fix or a product with no ERC. Those planning to stay long-term often benefit from the certainty of a five-year deal, particularly if rates are expected to rise during that period.

How much to borrow

If you are remortgaging to release equity, the amount you borrow affects your LTV and therefore your rate tier. Borrowing more pushes your LTV up, which may move you into a higher rate band and offset some of the saving you were expecting. A broker can model the optimal balance between equity release and rate impact.

How a Remortgage Broker Helps in Edinburgh

A whole-of-market remortgage broker Edinburgh does more than find a lower rate. The value is in the complete picture.

Whole-of-market access. Not all mortgage products are available direct to consumers. Broker-exclusive rates and products from lenders who do not operate direct-to-consumer channels are only accessible through an adviser. In some cases, these products are meaningfully better than anything on a comparison site.

Lender matching. Not every lender treats the same income profile identically. Self-employed applicants, those with complex income structures, or those with any credit history considerations will find that certain lenders are considerably more suitable than others. Applying to the wrong lender can result in a declined application or a lower offer than your profile supports.

Full cost comparison. Comparing mortgage rates without accounting for arrangement fees, cashback offers, and ERC costs gives an incomplete picture. A broker models the total cost of each option over the deal period, not just the headline rate.

Scottish legal process management. An Edinburgh broker familiar with remortgaging in Scotland can coordinate with your solicitor, manage the standard security process, and keep the transaction moving on the right timeline for your deal expiry date.

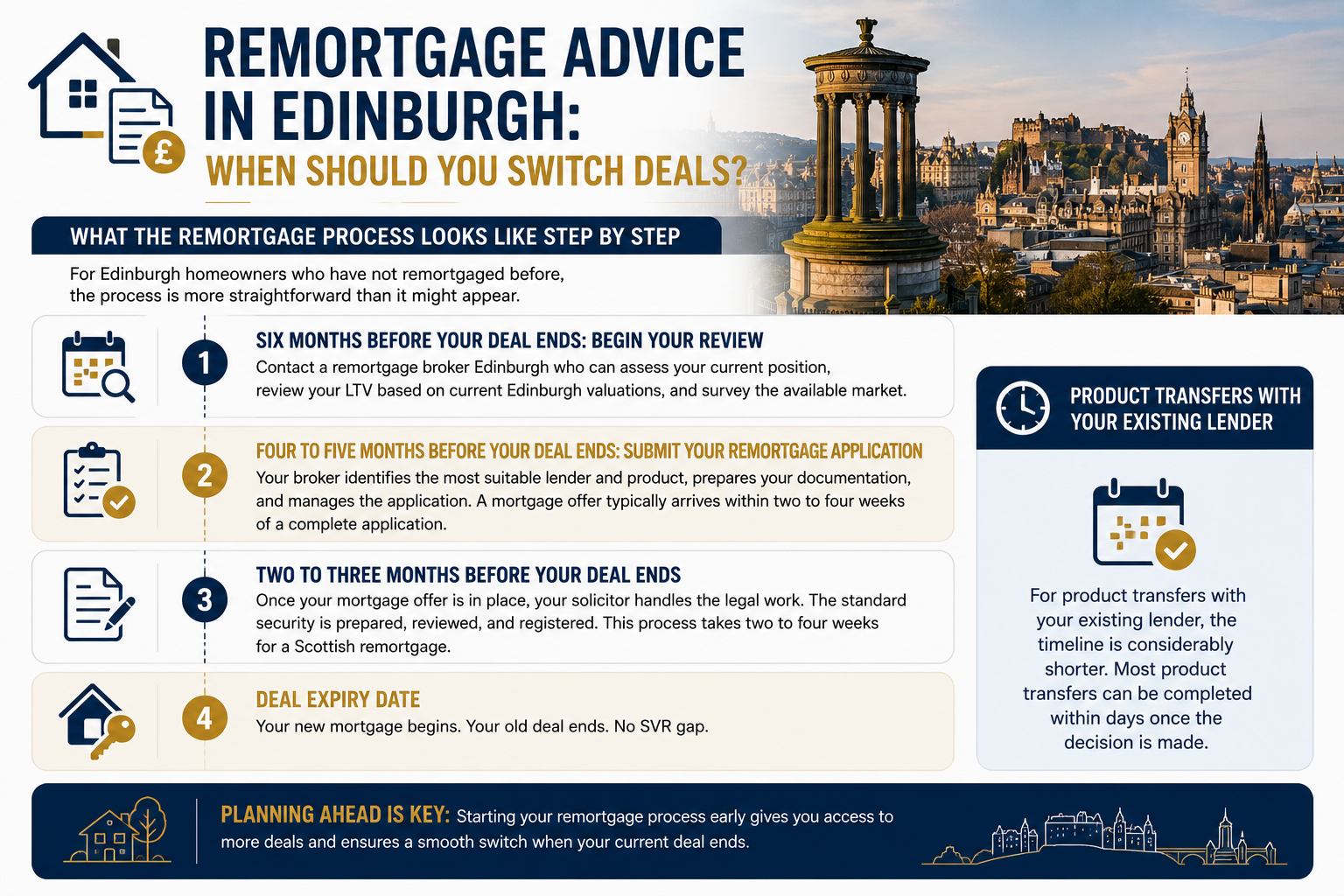

What the Remortgage Process Looks Like Step by Step

For Edinburgh homeowners who have not remortgaged before, the process is more straightforward than it might appear.

Six months before your deal ends: Begin your review. Contact a remortgage broker Edinburgh who can assess your current position, review your LTV based on current Edinburgh valuations, and survey the available market.

Four to five months before your deal ends: Submit your remortgage application. Your broker identifies the most suitable lender and product, prepares your documentation, and manages the application. A mortgage offer typically arrives within two to four weeks of a complete application.

Two to three months before your deal ends: Once your mortgage offer is in place, your solicitor handles the legal work. The standard security is prepared, reviewed, and registered. This process takes two to four weeks for a Scottish remortgage.

Deal expiry date: Your new mortgage begins. Your old deal ends. No SVR gap.

For product transfers with your existing lender, the timeline is considerably shorter. Most product transfers can be completed within days once the decision is made.

Frequently Asked Questions

Should I remortgage in Edinburgh?

You should review your mortgage position in Edinburgh if any of the following apply: your current fixed-rate deal ends within six months; you are already on your lender's SVR; your property has increased in value and you have not checked whether a lower LTV band is now available to you; or your circumstances have changed in a way that affects your affordability or product eligibility. Edinburgh's strong price growth since 2015 means many homeowners are in a significantly better LTV position than they were when they originally mortgaged, which can unlock better rates even if they have not made additional capital repayments.

When is the best time to remortgage in Edinburgh?

The best time to remortgage in Edinburgh is three to six months before your current deal ends. This window allows your broker to survey the market, submit an application, and have a new mortgage offer in place before your existing rate expires. Starting earlier rather than later protects you from processing delays and gives you time to compare options thoroughly. Most lenders allow you to lock in a new rate up to six months before the deal begins, so the new rate starts on day one of your new term with no period on the SVR.

How does remortgaging in Scotland differ from England?

Remortgaging in Scotland requires a solicitor to handle the title and security transfer, which is not always the case in England. When you switch to a new lender, the standard security held by your old lender must be discharged and a new one registered in favour of the incoming lender. This is a legal step specific to Scots property law. It typically adds two to four weeks and a solicitor's fee of £300 to £600 to the process. If you stay with your existing lender via a product transfer, the process is simpler and usually requires no solicitor. A remortgage broker Edinburgh familiar with Scottish conveyancing can manage this process alongside your application.

How much can I save by switching mortgage deals in Edinburgh?

The saving depends on your outstanding balance, current rate, and what deal is available. As a working example: an Edinburgh homeowner with £220,000 outstanding on a SVR of 6.83% who switches to a five-year fix at 4.5% would save approximately £269 per month, or around £3,228 per year. Over a five-year term, that is approximately £16,140 in lower interest payments, before accounting for the differences in capital repayment. The actual saving for your situation depends on your specific balance, term remaining, property value, and credit profile. A broker can model this precisely before you commit to anything.

Can I remortgage in Edinburgh to release equity?

Yes. Many Edinburgh homeowners use remortgaging to release equity built up through mortgage repayments and the city's strong price growth. Edinburgh's average house price has grown by approximately 51% since 2015. A homeowner who bought at £200,000 in 2016 and whose property is now worth £295,000 holds substantially more equity than they originally did. A remortgage at a higher loan amount releases some of that equity as cash, which can fund home improvements, repay other debts, or cover significant expenditure. The key consideration is that the additional borrowing is secured against your property, and the total cost over the mortgage term should be modelled carefully before proceeding.

How do I find the best remortgage deal in Edinburgh?

Using a whole-of-market remortgage broker Edinburgh gives you access to the full lending market, including broker-exclusive products not available on comparison sites. The best deal is not always the one with the lowest headline rate: arrangement fees, cashback, and ERC structures all affect the total cost over the deal period. A broker compares the full cost of each option against your specific balance, LTV, income, and plans for the property, and recommends the product that produces the best financial outcome for your circumstances, not just the one with the most attractive number on a rate table.

Final Thoughts

Edinburgh homeowners are in an unusually strong position for a remortgage review in 2025. Strong property price growth has improved LTV positions across the city. The Bank of England base rate has fallen from its 2023 peak. And a significant number of homeowners whose fixed deals were arranged during the low-rate period of 2020 to 2022 are now either approaching the end of those deals or have already moved onto their lender's SVR.

The cost of not reviewing is concrete and monthly. The cost of reviewing is a conversation.

Pelican Finance offers remortgage Edinburgh advice with whole-of-market access, full cost comparison across products and lenders, and a thorough understanding of how Scottish remortgaging works from application through to standard security registration. If your deal is ending, your property has grown in value, or you simply have not reviewed your mortgage in the past two years, a conversation costs nothing and typically reveals options worth taking.

Sources

- ONS Housing Prices: Edinburgh: Office for National Statistics, February 2026

- ESPC House Price Report: April to June 2025: Edinburgh Chamber of Commerce / ESPC

- ESPC House Price Report: May to July 2025: Edinburgh Chamber of Commerce / ESPC

- Edinburgh Property Market Review Late Summer 2025: Graham and Sibbald / ESPC Q3 2025 data

- Edinburgh Property Price Forecasts 2026: Investropa (Bank of England base rate data)

- Compare the Market: Average SVR: Compare the Market, March 2026

- Scottish Housing Market Review Q4 2025: Mortgage Interest Rates: Scottish Government

- Remortgaging in Scotland: Complete Legal Guide: Jones Whyte Solicitors

- Best Mortgage Rates in Scotland: Online Mortgage Advisor

Pelican Finance Limited is authorised and regulated by the Financial Conduct Authority (FCA register reference 731937). Your home may be repossessed if you do not keep up repayments on your mortgage. The information in this article is for general guidance only and does not constitute financial advice. Think carefully before securing other debts against your home.