May 7, 2026

First Time Buyer Mortgage Options in Paisley Explained

Paisley is one of the most accessible property markets in the west of Scotland for first-time buyers. Average prices sit well below the Scottish average, the town is around 20 minutes from Glasgow by train, and a growing range of mortgage products means the barrier to getting on the ladder here is lower than many buyers expect.

But accessible does not mean straightforward. The Scottish buying process, lender affordability rules, and deposit requirements all need to work together before a first time buyer mortgage Paisley application can succeed. This guide explains your options clearly, with current market data and practical steps you can act on.

Can You Get a Mortgage as a First-Time Buyer in Paisley?

Yes. First-time buyers in Paisley are well-positioned to secure a mortgage, for one straightforward reason: the numbers work.

According to ONS housing data for Renfrewshire, the average price paid by first-time buyers in Renfrewshire was £130,000 in February 2026, up 7.2% year on year. Rightmove records the overall average sold price in Paisley at £167,131 over the last year, with flats selling for an average of £107,022. These figures place Paisley firmly within reach for buyers with a 5% to 10% deposit, particularly those purchasing a flat or terraced property.

Compare that with the Scottish first-time buyer average of £153,000, and Paisley's entry point sits comfortably at or below the national benchmark. For a buyer targeting a flat at £107,000, a 10% deposit means saving £10,700, a realistic target for most working adults saving consistently over two to three years.

The question for most Paisley buyers is not whether a mortgage is possible. It is which product best fits their income, deposit, and the specific property they want to buy.

What Mortgage Options Are Available to First-Time Buyers in Paisley?

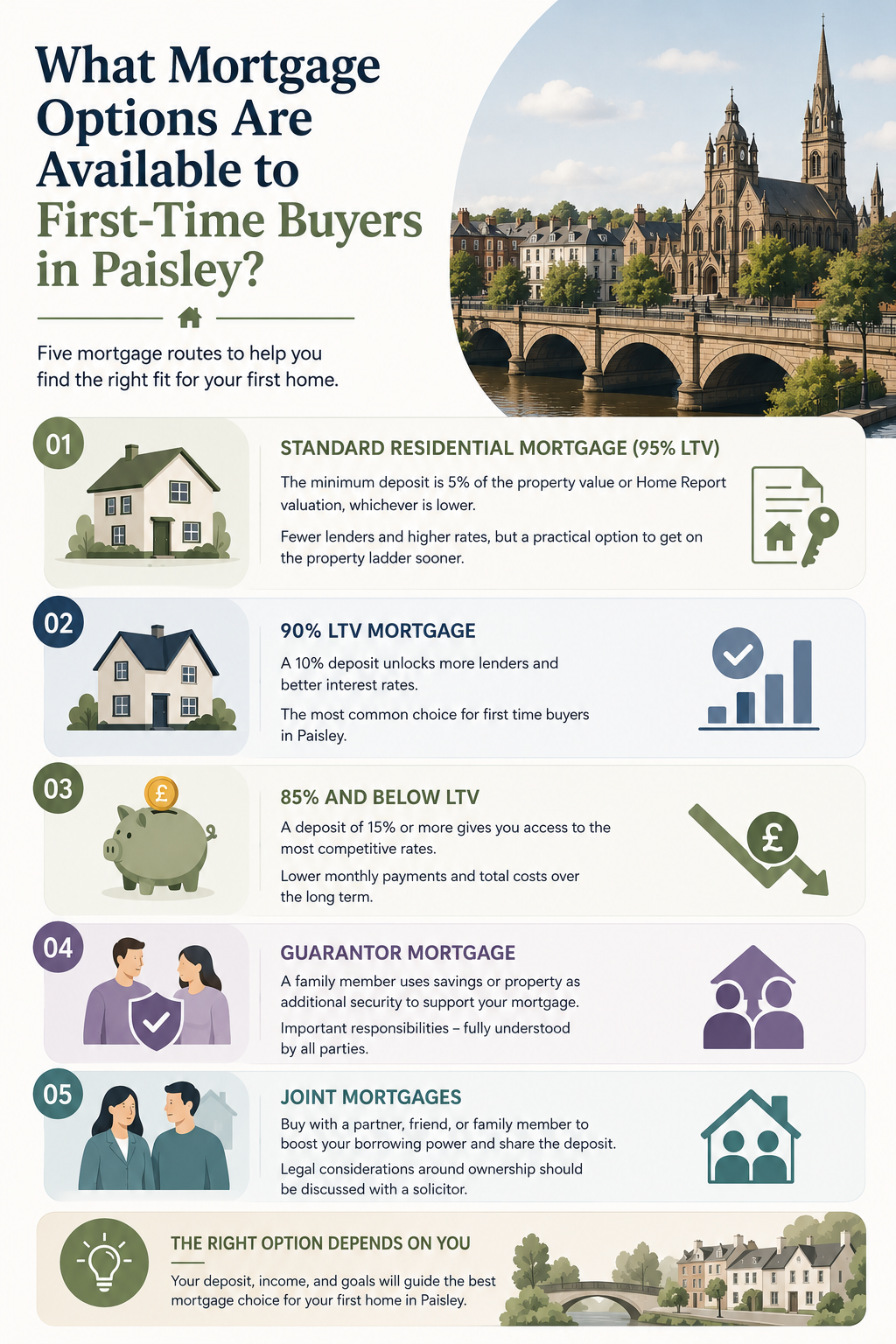

First time buyer mortgage Paisley options broadly fall into five categories. Understanding what each offers, and what it requires, helps you match your profile to the right product before you apply.

Standard Residential Mortgage (95% LTV)

The minimum deposit most lenders accept is 5% of the property's value or Home Report valuation, whichever is lower. At Paisley's flat average of £107,022, a 5% deposit is approximately £5,350.

At 95% LTV, the range of available lenders is narrower and interest rates are higher than at lower LTV bands. But buying home who have saved a smaller deposit and want to get onto the property ladder now rather than waiting years to accumulate more, this tier is a working option. Properties in Paisley at this price point are affordable enough that even higher-rate products remain manageable on a typical local income.

90% LTV Mortgage

Stepping up to a 10% deposit, around £10,700 on the Paisley flat average, unlocks significantly more lenders and more competitive rates. This is the most commonly recommended starting point for first time buyer mortgage Paisley applications because it balances achievable savings targets with meaningful product choice.

Most mainstream lenders, including those with the fastest turnaround times for Scottish purchases, operate comfortably at 90% LTV. For buyers targeting Paisley properties in the £130,000 to £160,000 range, a 10% deposit of £13,000 to £16,000 is the practical savings goal.

85% and Below LTV

Buyers who can save 15% or more gain access to the most competitive mortgage rates on the market. The monthly payment difference between a 95% LTV product and an 85% LTV product over a 25-year term on a £130,000 Paisley mortgage can be meaningful over the full mortgage term, even if it looks modest month to month.

If your timeline allows for additional saving, moving from 90% to 85% LTV is usually worth modelling with a broker before you decide when to buy.

Guarantor Mortgage

If your deposit is limited or your income alone is insufficient to borrow the amount you need, some lenders offer guarantor mortgages where a family member uses their savings or property as additional security for your loan.

Guarantor mortgages come with important conditions. The guarantor takes on legal and financial responsibility for the mortgage if you cannot make repayments. That responsibility needs to be fully understood by everyone involved before the application proceeds. A mortgage broker Paisley can explain how guarantor products currently work with specific lenders and what documentation is required.

Joint Mortgages

Buying with a partner, friend, or family member is a straightforward way to increase borrowing capacity and split deposit requirements. Most lenders assess joint applications on the basis of both incomes, which can significantly expand what is affordable in Paisley's market.

Joint ownership comes with legal considerations, particularly around what happens if circumstances change, that a solicitor should advise on separately from the mortgage process. Specialist legal and mortgage advice can help ensure both parties fully understand their rights, responsibilities, and long-term financial commitments before buying a property together.

How Much Can You Borrow as a First-Time Buyer in Paisley?

Lenders do not use simple salary multiples the way they once did. Each lender has its own affordability model that takes into account your gross income, your existing financial commitments, and how repayments would hold up if interest rates rose.

As a general guide, most lenders will consider lending between 4 and 4.5 times your gross annual income. Some lenders will go to 5 or 5.5 times income for applicants with strong credit profiles, higher incomes, or in specific professional categories.

Using those figures against Paisley's market:

In Paisley, the amount you can borrow is usually based on a multiple of your gross annual income, typically around 4x to 4.5x salary depending on the lender and your financial circumstances.

A buyer earning around £25,000 per year may be able to borrow between £100,000 and £112,500, which is often suitable for purchasing most flats in the area.

With a salary of approximately £30,000, borrowing power could increase to around £120,000 to £135,000, opening up options such as flats and smaller terraced homes.

For buyers earning £35,000 annually, lenders may offer between £140,000 and £157,500, making many terraced properties in Paisley more affordable.

An income of £40,000 could support borrowing of around £160,000 to £180,000, giving access to a wider range of semi-detached properties.

Those earning around £50,000 per year may be able to borrow between £200,000 and £225,000, providing access to a much broader selection of homes across Paisley’s property market.

These are estimates only. The actual amount a lender offers depends on your credit score, outstanding debts, childcare costs, student loan repayments, and several other factors. Applying to the wrong lender, one whose affordability model is less suited to your specific profile, can result in a lower offer than your income would otherwise support.

This is one of the main reasons Paisley mortgage advice from a whole-of-market broker adds value that direct applications often miss.

LBTT: What First-Time Buyers in Paisley Need to Know

Scotland uses Land and Buildings Transaction Tax (LBTT) rather than Stamp Duty. For first-time buyers in Paisley, this is largely good news.

First-time buyer LBTT relief raises the nil-rate threshold from £145,000 to £175,000. Given that Paisley's average flat price sits at £107,022 and the average terraced property at £168,684, many first-time buyer purchases in Paisley fall below the £175,000 threshold entirely, meaning no LBTT is payable at all.

A buyer purchasing a flat at £110,000 pays zero LBTT. A buyer purchasing a terraced property at £165,000 also pays zero LBTT. This is a material advantage compared with buying in Edinburgh or Glasgow city centre, where virtually no first-time buyer properties qualify for full relief.

For Paisley purchases above £175,000, such as semi-detached properties averaging £225,484, LBTT applies at 2% on the portion between £175,001 and £250,000. On a £225,000 purchase, that works out to approximately £1,000 in LBTT after first-time buyer relief.

Your solicitor calculates and submits LBTT on your behalf on completion. It must be paid from your own funds separately from the mortgage.

How the Scottish Buying Process Affects Your Mortgage as a First-Time Buyer in Paisley

Scotland's property buying system works differently from England's, and those differences directly affect how a first time buyer mortgage Paisley application needs to be structured.

Home Reports

In Scotland, sellers are legally required to provide a Home Report before marketing a property. The Home Report includes a surveyor's valuation, a condition rating, and an energy performance certificate.

Your lender bases your mortgage on the Home Report valuation, not the price you offer. If you bid above the Home Report value, which happens regularly in popular Paisley neighbourhoods like Ralston and Hunterhill, the gap between valuation and offer price comes from your own funds, on top of your deposit.

At Paisley's price levels, premiums above Home Report value tend to be more modest than in Glasgow or Edinburgh. ESPC reported that across the wider Scottish market, buyers paid an average of around 101% to 102% of Home Report value in spring 2025. Planning a small buffer of £2,000 to £5,000 above your deposit is sensible in sought-after Paisley streets.

Closing Dates

When a Paisley property receives significant interest, the seller's solicitor may set a closing date: a fixed deadline by which all sealed offers must be submitted. You only get one chance to bid, without knowing what others are offering.

Acting confidently at a closing date requires knowing your borrowing ceiling in advance. An Agreement in Principle (AIP) from a lender who has reviewed your complete financial position, not a quick online estimate, is what makes submitting a competitive offer possible.

Missives and Legal Commitment

Once missives are concluded in Scotland, both buyer and seller are legally committed. Unlike England, there is no extended "subject to contract" period after an offer is accepted. Getting your mortgage confirmed before that point is essential.

This means the mortgage process in Scotland front-loads more preparation than buyers from England sometimes expect. Starting conversations with a mortgage broker Paisley before you begin viewing properties puts you in a much stronger position.

What Affects Whether Your First-Time Buyer Mortgage Application Succeeds

Lenders assess every application against a set of criteria. Understanding what they look for before you apply helps you identify and address any weaknesses.

Credit Profile

Your credit file is the single most visible indicator of how you have managed financial commitments in the past. Lenders check all three major credit reference agencies: Experian, Equifax, and TransUnion. Each holds different data, so checking all three before applying gives you a complete picture.

Common issues that affect Paisley first-time buyer applications include: missed or late payments on any credit product in the past two to three years; high credit utilisation on revolving credit such as credit cards; accounts registered at old addresses that no longer match your credit file; and payday loans in the past 12 months, which some lenders treat as an automatic decline trigger.

Most credit issues are fixable with time. Identifying them three to six months before you plan to apply gives you the opportunity to address them before a lender sees your file.

Income Documentation

Lenders verify income in different ways depending on how you are employed.

Employed applicants with permanent contracts typically need their two most recent payslips and their most recent P60. Agency workers and those on zero-hours contracts may face more scrutiny around income stability.

Self-employed applicants in Paisley, including sole traders and limited company directors, generally need two years of accounts and tax returns. Some lenders will consider applications from those with one year of self-employment history, but the product range is narrower. A broker familiar with self-employed mortgage criteria can identify which lenders are currently most receptive.

Deposit Source

Lenders require evidence of where your deposit came from. Personal savings are straightforward, requiring bank statements showing the accumulation of funds over time. Gifted deposits from family members require a signed gift letter confirming no repayment is expected and that the donor has no claim on the property. Inherited funds require appropriate documentation.

Deposits sourced from personal loans are not accepted. Any loan or credit facility taken out to fund a deposit will be treated as a liability in the affordability calculation, typically reducing what the lender will offer.

How a Mortgage Broker Improves Your Chances in Paisley

Applying directly to a single lender limits you to that lender's products, their affordability model, and their interpretation of your credit file. A whole-of-market mortgage broker Paisley reviews your application against the full lending market and matches you to lenders whose specific criteria fit your profile.

In practical terms, this makes a difference in several ways.

Lender selection

Not every lender processes Scottish purchases with the same efficiency. Some have underwriting teams less familiar with Home Report valuations or closing date timelines. A broker who regularly places Paisley mortgages knows which lenders perform well for Scottish purchases and which to avoid for time-sensitive applications.

Application preparation

A declined mortgage application stays on your credit file and can affect subsequent applications. Applying to the right lender first time, with complete and correctly structured documentation, protects your credit position.

Rate access

Whole-of-market brokers have access to products not available through direct channels. In some cases, exclusive rates through broker networks are meaningfully better than anything available directly to consumers.

Closing date confidence

When you need to act at a closing date within 48 to 72 hours, knowing your broker has already reviewed your complete application and can confirm your position quickly is not a minor convenience. It is often the difference between securing a property and losing it.

Steps to Buy Your First Home in Paisley

The process of going from "thinking about buying" to "keys in hand" in Paisley follows a clear sequence. Each step builds on the one before.

Step 1: Check your credit file. Request your report from Experian, Equifax, and TransUnion. Correct any errors. Address any issues before they affect a lender's decision.

Step 2: Assess your deposit and savings. Calculate your realistic deposit amount, accounting for property prices in the Paisley areas you want to buy in, any likely premium above Home Report value, and the additional costs of purchase (legal fees, LBTT if applicable, mortgage fees).

Step 3: Speak to a mortgage broker. Before you register with estate agents or start viewing, speak to a mortgage broker Paisley who understands the Scottish market. They can confirm your borrowing capacity, identify which lenders suit your profile, and flag any issues to address before a formal application.

Step 4: Secure an Agreement in Principle. Your broker will recommend submitting an AIP with an appropriate lender once your application is ready. This confirms your borrowing capacity in principle without a full credit search on your file, and signals to sellers and solicitors that you are a serious, prepared buyer.

Step 5: Engage a solicitor. In Scotland, a solicitor handles both the legal conveyancing and the submission of offers on your behalf. You need a solicitor in place before you make any offer on a property. Your broker can recommend solicitors experienced in Scottish residential property if needed.

Step 6: Find a property and make an offer. With your AIP confirmed and your solicitor instructed, you can view properties and make offers with confidence. Your solicitor advises on the appropriate offer level, and your broker confirms your mortgage position before the offer is submitted.

Step 7: Full mortgage application. Once an offer is accepted, your broker submits a full mortgage application to the lender. Processing typically takes between one and three weeks from submission, depending on the lender and how complete your documentation is.

Step 8: Mortgage offer and completion. Your lender issues a formal mortgage offer. Your solicitor handles the remaining legal work, concludes missives, and arranges the date of entry when you receive the keys.

Frequently Asked Questions

Can I get a mortgage in Paisley as a first-time buyer?

Yes. Paisley's property market is one of the more accessible in the west of Scotland for first-time buyers. According to ONS housing data for Renfrewshire, the average first-time buyer price in Renfrewshire was £130,000 in February 2026, which is below the Scottish average and within reach for buyers with a 5% to 10% deposit. Most mainstream lenders accept applications for properties at Paisley price levels, and a whole-of-market broker can identify which lenders are best suited to your specific income and credit profile.

What mortgage deposit do I need to buy in Paisley?

The minimum deposit accepted by most lenders is 5% of the Home Report valuation. At Paisley's flat average of approximately £107,000, a 5% deposit is around £5,350. For terraced properties averaging £168,684, a 5% deposit is around £8,400. Most buy first home Paisley Scotland buyers target 10% to access a wider product range and better rates. For a £130,000 purchase, a 10% deposit of £13,000 is the practical savings target for most buyers.

Do first-time buyers pay LBTT in Paisley?

Most do not. First-time buyer LBTT relief raises the nil-rate threshold to £175,000, and the majority of Paisley's most popular first-time buyer property types, including flats averaging £107,022 and terraced homes averaging £168,684, fall below that threshold. Buyers in this price range pay no LBTT at all. For purchases above £175,000, LBTT applies at 2% on the portion above the threshold. On a £200,000 purchase, that works out to approximately £500 in LBTT after relief.

How long does it take to get a mortgage in Paisley?

An Agreement in Principle can typically be issued within 24 to 48 hours of submitting a complete application to a broker. A full mortgage offer, once the property is identified and the application submitted, typically takes one to three weeks depending on the lender. More complex applications, such as those involving self-employed income, previous credit issues, or non-standard property types, take longer. Working with a broker who prepares documentation thoroughly before submission compresses timelines and reduces the likelihood of delays.

Is Paisley a good place to buy a first home?

Paisley consistently ranks as one of the better-value options for first-time buyers in the west of Scotland. Average property prices are below the Scottish average, the LBTT position is favourable for most buyer budgets, and the commuter connection to Glasgow makes it an attractive location for professionals working in the city. Rightmove data shows Paisley prices rose 9% over the last year, suggesting steady capital growth alongside the affordability advantage. Areas such as Ralston, Hunterhill, and Gallowhill are among the most popular with buyers looking for space and value within the town.

What Paisley mortgage advice should I get before buying?

The most valuable advice at the planning stage covers four areas: confirming your realistic borrowing capacity with the lenders most suited to your profile; identifying and addressing any credit or income documentation issues before you apply; planning your deposit to account for above-Home Report-value offers and additional purchase costs; and understanding how the Scottish buying system works so you can act quickly when the right property appears. A whole-of-market broker covers all of these in an initial consultation, which at Pelican Finance costs nothing.

Final Thoughts

Paisley offers first-time buyers in the west of Scotland a rare combination: genuine affordability, strong transport links to Glasgow, a LBTT position that often means no tax at all, and a property market that has shown steady price growth. Whether you are buying your first home, exploring Rental properties, or planning your next move, Paisley continues to attract buyers looking for value and long-term potential.

The mortgage process, like any property purchase in Scotland, rewards preparation. Buyers who speak to a mortgage broker Paisley before they start viewing, get their documentation in order, and secure an Agreement in Principle early in the process consistently have better outcomes than those who try to put everything together after finding a property they want. Access to Specialist mortgage advice can also help buyers understand options around affordability, Protection, and future Remortgaging opportunities.

Pelican Finance works with first time buyer mortgage Paisley clients and buyers across the west of Scotland, offering whole-of-market advice and practical support through every stage of the purchase. If you are planning your first home in Paisley and want to understand your options, a conversation costs nothing and typically saves considerably more, while making the process simple from start to finish.

Sources

- ONS Housing Prices: Renfrewshire — Office for National Statistics, February 2026

- Rightmove House Prices: Paisley — Registers of Scotland data via Rightmove, April 2026

- Scottish Housing Market Review Q2 2025 — Scottish Government / UK HPI

- UK House Price Index Scotland: February 2026 — HM Land Registry / ONS

- ESPC House Price Report: March–May 2025 — Edinburgh Chamber of Commerce / ESPC

- LBTT Calculator and First-Time Buyer Relief — Savills / Revenue Scotland rates 2025/26

- Paisley Property Market Update Summer 2025 — Martin & Co Paisley

Pelican Finance Limited is authorised and regulated by the Financial Conduct Authority (FCA register reference 731937). Your home may be repossessed if you do not keep up repayments on your mortgage. The information in this article is for general guidance only and does not constitute financial advice.